The ETF Tax-Time Guide: Everything You Need for Your 2026 Tax Return

Tax season opens July 1. Your AMMA statements will arrive between July and August. And if you own VAS, VGS, VDHG, A200, or any other ASX-listed ETF — this guide is for you.

Most Australian ETF investors get their tax wrong. Not dramatically wrong, not obviously wrong, but wrong enough that the errors compound into thousands of dollars over a decade of investing. The mistakes are almost always the same five: trusting MyTax pre-fill blindly, missing foreign tax offsets, not tracking cost base adjustments, ignoring DRP parcels, and defaulting to FIFO when parcel selection would save them money.

This guide covers all of it. It uses real distribution data from Australia's largest ETFs — VAS, A200, VGS, VDHG, and VHY — and explains the mechanics behind the AMMA statement in plain language. By the end, you'll know exactly what to put in your tax return, where the numbers come from, and how to avoid the mistakes that silently inflate your tax bill year after year.

The Basics: How ETF Tax Works in Australia

Australian ETFs are structured as unit trusts and operate under the AMIT regime — the Attribution Managed Investment Trust framework introduced by the Australian government. Understanding this one concept unlocks everything else.

You're Taxed on Attributed Income, Not Cash Received

This is the single most important thing to understand about ETF tax in Australia, and it's the source of most confusion.

When an ETF earns income — from dividends, interest, rent, or capital gains on internal trades — that income is attributed to you as a unitholder, whether or not the fund actually distributes it as cash. The AMIT regime allows funds to attribute specific amounts of each income type directly to each investor, based on units held.

VanEck explains it this way: "The ETF dividend isn't taxable, it is the attribution on the AMMA statement that is taxable. Company dividends are the passing on of post-tax profits whereas ETF dividends are the passing on of pre-tax profits."

This means you could receive $900 cash in distributions but be taxed on $1,000 of attributed income — because the fund attributed $1,000 to you for tax purposes, and the difference adjusts your cost base. Equally, in some years the cash you receive might exceed your taxable attribution. The ATO's AMIT cost base guidance explains the mechanics in detail, but the practical takeaway is simple: the AMMA statement is your primary tax document, not your broker statement, not your bank statement.

The AMMA Statement Is Your Source of Truth

Your broker statement shows cash flows. Your bank statement shows what landed in your account. Your AMMA statement — the AMIT Member Annual statement — shows what you owe tax on.

These three numbers are often different. Always use your AMMA statement. As Illuminvest notes: "The AMMA statement is the primary document for correctly reporting ETF investment income in your tax return and for updating your cost base."

AMMA statements are issued by each ETF provider — Vanguard, BetaShares, iShares, VanEck, Global X — typically in July or August for the financial year just ended. You receive one per ETF per year.

For a deeper foundation, see ETF Tax in Australia: Franking Credits, Distributions and What You Actually Owe.

What's on Your AMMA Statement

The AMMA statement can look intimidating. It isn't once you understand what each line means. Here's a walk-through using VAS as the primary example — VAS is Australia's largest ETF by assets and has one of the most representative AMMA statements for a domestic equity fund.

1. Australian Dividends

This is the dividend income the fund collected from its underlying Australian share holdings — BHP, CBA, CSL and ~300 others — and attributed to you. VAS distributes approximately $3.40 per unit per year in total distributions, of which Australian dividends make up the largest component.

You report this as trust income (Label 13 in your tax return), not as a direct dividend. The gross amount includes the attached franking credits, which you claim separately.

2. Franking Credits

Australian companies pay tax at the corporate rate (30%, or 25% for smaller companies) before distributing dividends. Franking credits represent that pre-paid tax and flow through to you as an ETF investor — you can use them to offset your personal tax liability, or receive them as a refund if your marginal rate is below the corporate rate.

VAS runs at approximately 74.83% franked (as reported for calendar year 2025 by The Bull's VAS ETF Guide). In practical terms: for every $1 of Australian dividend income from VAS, around $0.75 is accompanied by a franking credit. The June 2025 distribution carried approximately $0.46 per unit in franking credits. Those credits can be life-changing for low-income investors and SMSF pension accounts — more on this in the Franking Credits section below.

3. Foreign Income + Foreign Income Tax Offset (FITO)

This is the territory of VGS, BGBL, IVV, and other international ETFs. When those funds collect dividends from Microsoft, Apple, Nestlé or Toyota, those dividends have already been taxed in the US, Europe, or Japan via withholding tax. That withholding tax generates a Foreign Income Tax Offset (FITO) — a credit that offsets the Australian tax you would otherwise owe on the same income.

SPDR's tax guide explains: "Your ETF AMMA statement will show the gross amount of foreign income (label 20E). The foreign income tax offsets may only be used to the extent to which they offset the [Australian tax payable on that income]."

Report foreign income at Label 20E and claim the FITO at Label 20O. Missing the FITO means paying Australian tax on top of foreign withholding tax — you're effectively taxed twice on the same dollar.

4. Capital Gains (Discounted and Non-Discounted)

ETFs trade their underlying holdings throughout the year. When the index rebalances — adding new stocks, removing old ones — the fund sells shares and realises capital gains. Those gains are passed through to you on the AMMA statement, even if you didn't sell a single ETF unit yourself.

There are two categories:

Discounted capital gains: from assets held by the fund for more than 12 months. You're entitled to the 50% CGT discount — but the ETF applies it at the fund level before attribution. The amount shown on your AMMA statement is already the discounted amount.

Non-discounted capital gains: short-term gains (assets held less than 12 months inside the fund). No discount applies. Taxed at your full marginal rate.

VAS had approximately $0.46 per unit in discounted capital gains in the June 2023 distribution (as reported in Reddit's r/fiaustralia discussion of Vanguard's June 2023 breakdown: $0.814 income + $0.464 discounted CG per unit).

Report capital gains from distributions at Label 18 in your tax return.

5. Tax-Deferred / Return of Capital

Some ETFs distribute amounts that are not immediately taxable — because the underlying income is structured as a return of capital or is deferred under tax rules. This is most common in property ETFs like VAP and infrastructure funds. The cash lands in your account, but it's not income — it's your own money being returned.

The catch: tax-deferred distributions reduce your cost base. You're not taxed now, but when you eventually sell, your reduced cost base creates a larger capital gain. As Illuminvest explains: "When an ETF distribution includes tax-deferred or return of capital amounts, your cost base must be reduced by that amount. Failing to track these adjustments leads to incorrect capital gains calculations when you eventually sell."

6. AMIT Cost Base Adjustment

This is the most misunderstood section of any AMMA statement. It appears on the last page and typically shows a small positive or negative dollar amount per unit. Investors often ignore it. They shouldn't.

VanEck's explanation cuts to the core of why it exists: "The amount shown on your AMMA statement as an increase or decrease in your cost base is just the difference between the taxable amounts on the AMMA statement and the amount of cash you received as a dividend. It's not really a 'benefit'. It's just ensuring that when you finally sell the ETF units, the amount of capital gain will be calculated to accurately reflect the true profit on your investment."

In plain English: if you were taxed on more income than you received in cash, your cost base goes up (reducing future capital gains). If you received more cash than you were taxed on, your cost base goes down (increasing future capital gains). The adjustment is deemed to occur on 30 June each year, and it must be applied pro-rata across every parcel you held on that date.

According to the ATO's cost base guidance: "The cost base of your units in the AMIT can be adjusted both upward and downward." Upward adjustments were not previously allowed under the old trust regime — this is one of the key benefits the AMIT framework introduced.

Distribution Profile Summary: Top 5 ETFs

ETF | Australian Dividends | Franking | Foreign Income | FITO | Capital Gains | Tax-Deferred |

|---|---|---|---|---|---|---|

High | High (~75%) | Minimal | Minimal | Moderate | Low | |

High | High (~80%) | None | None | Low | Low | |

None | None | High | Moderate | Moderate | Low | |

Mixed | Moderate (~40%) | Moderate | Moderate | High (rebalancing) | Moderate | |

High | Very High (~80%) | Minimal | Minimal | Low | Low |

The 5 Most Common ETF Tax Mistakes

These five mistakes account for the majority of errors in Australian ETF tax returns. None of them are obscure edge cases — they affect everyday investors holding mainstream ETFs in standard brokerage accounts.

Mistake 1: Relying on MyTax Pre-Fill Without Checking

MyTax pre-fill is convenient. It pulls data from fund managers and investment platforms directly into your tax return. The problem: it often arrives late, covers incomplete periods, uses different classification than your AMMA statement, or simply contains errors.

Pre-fill data is also not guaranteed to match your AMMA statement. Fund managers report to the ATO, and the ATO populates your return — but timing lags mean pre-fill data can be available before final AMMA statements are issued, creating mismatches. The ATO itself notes that pre-fill is a guide, not a substitute for your own records.

What to do instead: Download your AMMA statements directly from each fund provider's website — Vanguard's investor portal, BetaShares' tax page, the iShares/VanEck equivalents. Cross-check every line against what MyTax has pre-filled. The AMMA statement wins every time there's a discrepancy.

Mistake 2: Ignoring Foreign Tax Offsets (FITO)

If you hold VGS, BGBL, NDQ, or any international equities ETF, you're entitled to a Foreign Income Tax Offset. Without it, you pay full Australian marginal tax on income that has already been partially taxed overseas.

The FITO is right there on your AMMA statement — it requires no special calculation, no complex form, no accountant to claim. You enter the gross foreign income at Label 20E and the foreign tax offset amount at Label 20O. That's it. Yet this is one of the most frequently missed items in ETF tax returns.

The amount varies by fund. For VGS, the FITO is typically moderate relative to foreign income, reflecting US withholding tax primarily. For ETFs with broader geographic exposure, it includes withholding taxes from multiple jurisdictions.

Mistake 3: Not Tracking AMIT Cost Base Adjustments

This is the mistake that costs investors the most money over the long term — precisely because the annual impact appears small. A cost base reduction of $0.08 per unit in year one is easy to ignore. After ten years of ignoring it, with a cost base that's understated by $0.80+ per unit across dozens of parcels, the error materialises as a significantly overstated capital gain the year you sell.

As Illuminvest explains: "Example: You hold 500 units with a cost base of $20.00 per unit (total cost base: $10,000). The AMMA statement shows a cost base reduction of $0.15 per unit. Updated cost base per unit: $20.00 − $0.15 = $19.85. Updated total cost base: 500 × $19.85 = $9,925."

The complexity compounds for dollar-cost averagers. If you've been buying VAS monthly for three years, you have 36 purchase parcels. The annual cost base adjustment must be applied pro-rata across all 36 parcels based on units held on 30 June. This is precisely what makes software like Sharesight or Navexa worth using — they automate the pro-rata calculation across every parcel automatically.

The annual process: After each AMMA statement:

Identify the cost base adjustment per unit (positive or negative)

Apply it proportionally to every parcel you held on 30 June

Update your records (spreadsheet, Sharesight, or Navexa)

Keep the AMMA statement — you'll need it when you sell, potentially years later

Mistake 4: Forgetting That DRP Creates New Parcels

Dividend Reinvestment Plans are attractive — you don't have to pay brokerage, and your holding grows automatically. But every DRP reinvestment is a new acquisition at a new price point, and each one creates a new cost base parcel.

If you've participated in DRP for five years with quarterly distributions, you may have 20+ additional parcels on top of your original purchases. Each parcel has its own cost base (the market price on the DRP reinvestment date) and its own acquisition date (which matters for the 12-month CGT discount).

When you eventually sell, you need the cost base of every single parcel. If you can't produce it, you'll either overpay on CGT or face an ATO audit. The solution is either tracking software or switching off DRP and using the cash distributions to manually reinvest (which consolidates control at the cost of some admin friction).

Mistake 5: Not Knowing FIFO vs Specific Parcel Selection

When you sell ETF units, you need to identify which parcels you're selling. The default assumption — and the one many accountants use without thinking — is FIFO (First In, First Out): the oldest parcels are deemed sold first.

FIFO is not mandatory. You can choose specific parcel identification, selecting exactly which parcels to sell. This is perfectly legal and is explicitly supported by the ATO's CGT calculation guidance.

Why does it matter? Your oldest parcels — bought years ago at lower prices — likely have the highest capital gains. Your most recent parcels may have little or no gain, or even a loss. Selling high-cost-base parcels first minimises the capital gain in the current year. Selling parcels acquired less than 12 months ago can crystallise losses without surrendering the 50% CGT discount on other gains.

The practical applications:

VAS held since 2015: FIFO forces you to sell the 2015 parcels first (massive gain). Specific ID lets you sell 2024 parcels first (minimal gain).

Tax-loss harvesting scenario: You can select parcels that are at a loss to offset gains from other investments elsewhere in your portfolio.

What Each Type of ETF Means for Your Tax Return

Not all ETFs produce the same type of tax liability. The asset class underneath the ETF largely determines what appears on your AMMA statement — and how that affects your personal tax position.

Australian Shares ETFs: VAS, A200, IOZ

Australian equity ETFs produce the most investor-friendly tax profile for most Australians. The distributions are predominantly franked dividends — income that has already had corporate tax paid on it — meaning you receive a credit for that pre-paid tax.

VAS runs approximately 75% franked. A200, which tracks a similar but slightly more concentrated Australian index, typically runs around 80% franked due to its heavier weighting in large-cap dividend payers. IOZ from iShares tracks the ASX 200 with broadly similar characteristics.

Capital gains distributions from these funds are moderate — index rebalances generate some, but the Australian index doesn't turn over dramatically. AMMA statements for these ETFs are relatively straightforward compared to their international counterparts.

For a detailed comparison of the three main Australian equity ETFs, see VAS vs A200 vs IOZ: Which Australian Shares ETF Is Best?

International Shares ETFs: VGS, BGBL, IVV

International ETFs produce no franking credits — there's no Australian corporate tax involved. Instead, the dominant components are foreign income and the associated FITO.

VGS from Vanguard and BGBL from BetaShares both track global developed markets and produce broadly similar AMMA statement profiles. Both are unhedged, which means currency movements affect your economic exposure — but importantly, currency movements themselves don't directly affect the AMMA statement. They do affect your cost base calculation when you eventually sell, because your cost base is recorded in AUD at the time of purchase, and the AUD value of your units changes with exchange rates.

The FITO is the critical item to claim. International ETFs typically carry moderate FITO relative to their foreign income distributions — reflecting primarily US withholding tax (usually 15–30% depending on treaty arrangements) and lesser amounts from other jurisdictions.

For a deep comparison of the two largest international ETFs in Australia, see VGS vs BGBL: Which International Shares ETF Should You Buy?

For the hedged vs unhedged tax implications, see Hedged vs Unhedged ETFs: When to Use Each and the Hidden Cost of Getting It Wrong.

Diversified / All-in-One ETFs: VDHG, DHHF, VDGR

Diversified ETFs hold everything — Australian shares, international shares, bonds, sometimes property — producing the most complex AMMA statements of any mainstream ETF category. Expect to see Australian dividends, franking credits, foreign income, FITO, capital gains, and sometimes tax-deferred components all on the same statement.

VDHG deserves specific attention for a structural reason that materially affects tax outcomes. Unlike pure ETF structures, VDHG holds unlisted managed funds as its underlying components — not just ASX-listed ETFs. This distinction matters because, as Morningstar's deep dive into VDHG explains: "When investors exit an unlisted fund, they're paid out in cash. If fund managers sell assets to get that cash, it can create capital gains for the fund's remaining investors. Those gains are passed on to investors as a taxable distribution."

This is why VDHG consistently generates higher capital gains distributions than DHHF, which holds only ASX-listed ETFs as its underlying components. DHHF's ETF-of-ETFs structure allows capital gains from investor redemptions to be "streamed" to market makers rather than remaining investors — a meaningful tax efficiency advantage. Morningstar confirms that differences between the unlisted fund and ETF versions of the same Vanguard strategy range from "a few tenths of a percent to more than two [percent in annualised distribution yield]."

For investors in the accumulation phase who want a simple all-in-one fund and prefer to minimise annual tax drag, DHHF is generally more tax-efficient than VDHG on this basis.

For a full comparison, see VDHG vs DHHF vs GHHF: Which All-in-One ETF Should You Buy?

Dividend / Income ETFs: VHY, SYI, IHD

Dividend-focused ETFs deliberately select high-yielding Australian companies — often banks, insurers, and resources companies — which also tend to carry high franking levels. VHY from Vanguard typically runs around 80% franked, and IHD from iShares runs approximately 65%.

In low tax brackets, or for SMSF pension accounts where the effective tax rate is 0%, the high franking on these funds generates meaningful cash refunds from the ATO. For a $50,000 holding in VHY, the franking credits alone could generate a refund of several hundred dollars — entirely from holding a mainstream ETF.

For a full review of Australia's dividend ETF landscape, see Australia's Dividend ETFs Exposed: Same Promise, Very Different Results.

Bond / Fixed Income ETFs: IAF, SUBD, AAA

Bond ETF distributions are interest income — taxed at your full marginal rate with no CGT discount, no franking credits, no foreign tax offsets (in most cases). From a tax perspective, they're the least efficient vehicle for high-income earners, but entirely appropriate for low-income investors, retirees, or SMSF funds where the tax rate is low or zero.

AAA and similar cash/short-duration ETFs are especially straightforward — distributions arrive monthly, are classified entirely as interest income on the AMMA statement, and require only one line on your tax return.

SUBD (subordinated debt ETF) may include small tax-deferred components depending on the nature of the instruments held. As always, check the AMMA statement.

Property / REIT ETFs: VAP, REIT

Property ETFs and REIT ETFs are the category where tax-deferred distributions are most common and most significant. VAP from Vanguard, for example, holds Australian property trusts (A-REITs) that themselves distribute a mix of income and tax-deferred amounts. Depending on the underlying REITs and financial year, the tax-deferred component can represent 20–40% of total distributions.

This tax-deferred amount is cash in your hand — but it reduces your cost base rather than triggering immediate tax. The day you sell, that accumulated reduction materialises as a larger capital gain. For long-term holders of VAP who've received years of partially tax-deferred distributions without tracking them, the CGT calculation on eventual sale can be significantly higher than expected.

AMIT cost base adjustments for property ETFs can be larger in absolute dollar terms than for equity ETFs, making the tracking discipline even more important.

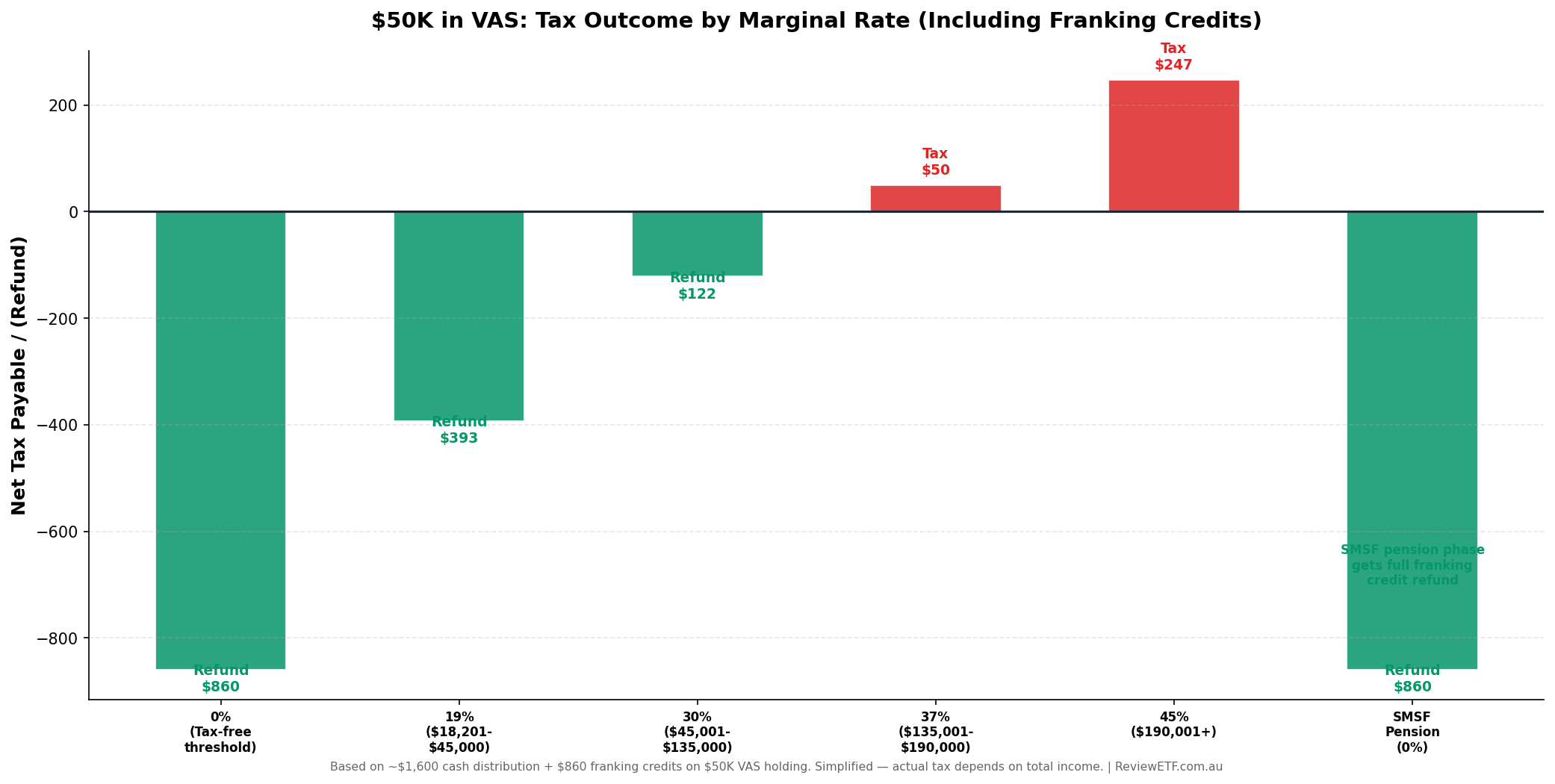

Franking Credits: The Full Picture

Franking credits are one of Australia's most distinctive and valuable tax features — and one of the most misunderstood. For ETF investors, the practical question is simple: given my marginal tax rate, what does VAS's franking profile actually mean for my tax bill?

Here's a worked example using a $50,000 holding in VAS:

Assumptions: VAS distributes approximately $1,600 of Australian dividend income per year on a $50,000 holding (3.2% yield), approximately 75% franked. Franking credits = $600. Gross dividend income including credits = ~$2,200. Franking credit amount = approximately $860 (calculated at 30% corporate tax rate on gross income).

Tax Bracket | Tax Rate | Tax on Gross Income | Franking Credit Offset | Net Tax / (Refund) |

|---|---|---|---|---|

Tax-free threshold | 0% | $0 | −$860 | ($860) refund |

Low-income earner | 19% | $418 | −$860 | ($442) refund |

Middle income | 30% | $660 | −$860 | ($200) refund |

Upper-middle | 37% | $814 | −$860 | ($46) refund |

Top bracket | 45% | $990 | −$860 | $130 tax |

SMSF pension (0%) | 0% | $0 | −$860 | ($860) refund |

The key insight: if you earn under approximately $135,000 (roughly the threshold where marginal rates make the credits a net cost rather than a benefit), VAS distributions effectively generate a tax refund thanks to franking. The credits offset not just the income tax on VAS distributions, but can also reduce tax payable on other income sources.

For SMSF funds in pension phase — where the effective tax rate is 0% — franking credits are refunded in full as cash. This makes high-franking ETFs like VAS, A200, and VHY particularly valuable assets for SMSFs in retirement phase.

The mechanics: you report the gross dividend (cash + franking credits) as income, add the franking credits to your tax payable as a credit, and the net result is the refund or tax shown above. This is handled automatically in MyTax — but the numbers must come from your AMMA statement, not the pre-fill.

For an in-depth look at how franking integrates with the full ETF tax picture, see ETF Tax in Australia: Franking Credits, Distributions and What You Actually Owe.

AMIT Cost Base Adjustments: The Worked Example

To make cost base adjustments concrete, here's a three-year example using VAS.

Starting position (July 2022): 500 units of VAS purchased at $90.00 per unit. Total cost base: $45,000.

Year 1 (FY2023 AMMA statement):

Cost base adjustment: −$0.20 per unit (net decrease — you received more cash than was attributed for tax).

Updated cost base: $90.00 − $0.20 = $89.80 per unit. Total: $44,900.

Year 2 (FY2024 AMMA statement):

Cost base adjustment: +$0.15 per unit (net increase — you were taxed on more than you received in cash; for example, a large capital gains attribution with modest cash distribution).

Updated cost base: $89.80 + $0.15 = $89.95 per unit. Total: $44,975.

Year 3 (FY2025 AMMA statement):

Cost base adjustment: −$0.18 per unit.

Updated cost base: $89.95 − $0.18 = $89.77 per unit. Total: $44,885.

Net effect after 3 years: Cost base reduced from $45,000 to $44,885 — a reduction of $115. If you sell at year 3 for $50,000, your capital gain is $5,115 (not the $5,000 you might have assumed). Small now — but over 20 years and across dozens of DCA parcels, the untracked adjustments can compound into thousands of dollars of understated or overstated cost base.

As VanEck explains: "If you later sell off the ETF units, across a number of future financial years, you will need to apportion the cost base adjustment on this year's AMMA statement across the ETF units that you held on 30 June [of that year]."

The practical implications for DCA investors are significant. Navexa's explainer video on AMIT cost base adjustments demonstrates precisely this: if you have 36 monthly purchase parcels, the adjustment divides by total units held and is applied across all 36 parcels proportionally.

Practical Tools for Tracking

Option 1 — Sharesight or Navexa: Both platforms import AMMA statements and apply cost base adjustments automatically across all parcels. This is the recommended approach for anyone with more than a handful of parcels or more than one or two ETFs.

Option 2 — Manual spreadsheet: Maintain a spreadsheet with one row per parcel, columns for purchase date, purchase price, units, and current cost base per unit. After each AMMA statement, add the adjustment amount to each row. Keep AMMA statements archived permanently — you'll need them when you sell, potentially 20 years from now.

Non-negotiable rule: Keep ALL AMMA statements, every year, for every ETF you hold. BetaShares' CGT guidance makes this explicit: "The information about cost base adjustments outlined on the AMMA statement should be retained by ETF investors and incorporated them into the cost base of your ETF investments."

Tax-Loss Harvesting: A Legal Way to Reduce Your Tax Bill

Tax-loss harvesting is the deliberate crystallisation of an unrealised capital loss in order to offset capital gains elsewhere in your portfolio. It's entirely legal, explicitly supported by ATO CGT rules, and significantly underused by Australian retail investors.

The mechanics: if you hold VGS at a loss — say, purchased units at $110 and they're now worth $95 — you can sell those units, crystallise a $15/unit capital loss, and use that loss to offset capital gains from other investments (other ETF sales, investment property, shares). The loss carries forward indefinitely until you have gains to offset.

The critical rule: you cannot immediately repurchase the same ETF. This is the "wash sale" prohibition — while Australia doesn't have a formal wash sale rule like the US, the ATO can treat transactions as having no economic substance if you sell and immediately rebuy an identical asset purely to manufacture a tax loss. The solution is to swap to an economically similar but not identical ETF:

Sold | Replacement | Index difference |

|---|---|---|

ASX 300 → ASX 200 (similar exposure, different index) | ||

ASX 200 → ASX 300 | ||

FTSE Developed → MSCI World (substantially similar, but different index) | ||

Different S&P 500 providers |

The swap maintains your market exposure with minimal tracking error while legitimately crystallising the loss. In periods of market drawdown — where your ETF portfolio might be sitting at a loss — this strategy can offset gains from other assets (an investment property sale, for example) and meaningfully reduce your total tax bill for the year.

For more on the fee and performance considerations that affect which ETF you swap to, see Is the Cheapest ETF Always the Best? We Tested Every Category.

Your Tax Return Checklist

Walk through these nine steps every year from July 1.

Step 1: Collect all AMMA statements

One statement per ETF per year. Download directly from each fund provider's website or investor portal. Don't wait for the mail or rely on your broker to provide them. Providers typically make them available by August — some earlier.

Step 2: Cross-check against MyTax pre-fill

Open your myGov account, access MyTax, and review what's been pre-filled. Check every number against your AMMA statements. If there are discrepancies, the AMMA statement takes precedence. Don't just click accept on pre-filled data.

Step 3: Report Australian dividends and franking credits (Label 13)

Enter the gross Australian dividend amount and the attached franking credit from your AMMA statement. The gross amount includes the credit — check your statement for the separate line items.

Step 4: Report foreign income and FITO (Label 20)

Gross foreign income at Label 20E. Foreign Income Tax Offset at Label 20O. This applies to every international ETF you hold — VGS, BGBL, NDQ, IVV, and others.

Step 5: Report capital gains from distributions (Label 18)

If your AMMA statement shows discounted capital gains, enter the grossed-up amount (double the discounted amount) as your gross capital gain, then apply the CGT discount in the calculation. For non-discounted capital gains, enter the full amount. Your AMMA statement should provide the amounts clearly.

Step 6: Update cost base records for each ETF

Before lodging, update your cost base spreadsheet or Sharesight/Navexa account with the AMIT cost base adjustment from each AMMA statement. Apply pro-rata across all parcels held at 30 June. File the AMMA statement for future reference.

Step 7: Calculate CGT if you sold ETF units during the year

If you sold any ETF units, calculate the capital gain or loss for each sale: proceeds minus adjusted cost base. Apply the 50% CGT discount if you held the parcel for more than 12 months. Net gains against any losses.

Step 8: Consider specific parcel identification

Before finalising CGT calculations, assess whether FIFO produces the optimal outcome. If selling high-cost parcels first reduces your gain, use specific identification — record which parcels you're selecting and retain that record.

Step 9: Lodge by October 31 (or later with a tax agent)

The standard lodgement deadline for individuals is October 31. If you use a registered tax agent, they have access to lodgement deferrals that can extend this significantly — useful if your affairs are complex or if AMMA statements arrive late.

Key Takeaways

Your AMMA statement is the source of truth — not MyTax pre-fill, not your broker statement, not your bank account.

Track AMIT cost base adjustments every year, even if you don't sell. Small adjustments compound over decades. Ignoring them means getting your CGT calculation wrong when it actually matters.

Franking credits generate refunds for anyone earning under approximately $135,000. VAS, A200, and VHY all run 75–80% franked. SMSF pension accounts receive the full credit refunded as cash.

FITO offsets for international ETFs prevent double taxation. VGS, BGBL, and NDQ holders: check Label 20 on your AMMA statement. Don't skip the offset.

DRP creates new parcels. Every reinvestment is a new purchase at a new price. Each one needs its own cost base — tracked from the reinvestment date.

VDHG generates larger capital gains distributions than DHHF because it holds unlisted managed funds, not just ASX-listed ETFs. If minimising annual tax drag matters, DHHF is structurally more efficient.

Tax-loss harvesting — VAS↔A200, VGS↔BGBL — is legal and effective. Crystallise losses in down markets, offset gains elsewhere, maintain market exposure. It costs almost nothing to implement.

Use Sharesight or Navexa. Manual tracking across 20+ parcels, multiple ETFs, and annual AMIT adjustments is genuinely error-prone. The cost of the software is small relative to a single year's tax error.

Resources and Sources

This guide draws on official and authoritative sources. Always verify the current year's specific figures using your own AMMA statements.

Morningstar: ETF deep dive — VDHG the multi-sector offering from Vanguard

SPDR: Guide to your State Street Global Advisors SPDR ETF Annual Tax Statement

Magellan: Understanding your AMIT Member Annual (AMMA) Statement

Navexa: How to Calculate AMIT Cost Base Adjustments (YouTube)

This article is general information only and does not constitute financial or tax advice. Consult a registered tax agent or financial adviser for advice specific to your circumstances.

Want more ETF analysis? Subscribe to the ETF Adviser Substack, watch the ReviewETF YouTube channel, or browse the full ETF database at ReviewETF.com.au.