ETF Tax in Australia: Franking Credits, Distributions, and What You Actually Owe

ETF distributions in Australia are more complex than dividends from a single company. You don't just receive cash — you receive a mix of franked dividends, unfranked dividends, capital gains, foreign income, and AMIT cost base adjustments. Each component is taxed differently. Getting it wrong means either overpaying the ATO or facing an audit.

This guide breaks down exactly how ETFs are taxed in Australia, how franking credits work, and which ETFs are the most tax-efficient.

How ETF Distributions Are Taxed

Unlike company shares where you receive a simple franked or unfranked dividend, ETFs distribute income through a trust structure. Most Australian ETFs operate under the AMIT (Attribution Managed Investment Trust) regime, which means the ETF's income is "attributed" to you whether or not it's actually paid out as cash.

Your annual AMMA statement (AMIT Member Annual statement) breaks your distribution into these components:

Component | How It's Taxed | Key Detail |

|---|---|---|

Franked dividends | Grossed-up then offset by franking credits | The tax has already been paid by the company at 30% |

Unfranked dividends | Added to taxable income at your marginal rate | No tax offset — you pay the full rate |

Discounted capital gains | Only 50% is taxable (if ETF held asset 12mo+) | Common when ETFs rebalance their holdings |

Non-discounted capital gains | 100% taxable at your marginal rate | Short-term trades within the ETF |

Foreign income | Taxable, but FITO may offset foreign tax paid | International ETFs like VGS have this |

Tax-deferred (NANE) | Not taxed now, reduces your cost base | Taxed as capital gain when you eventually sell |

AMIT cost base adjustment | Not taxed now, adjusts cost base up or down | Critical for calculating future CGT correctly |

The key principle: ETFs themselves don't pay tax. All income flows through to you, the unitholder. Your AMMA statement tells you what to declare — and it may be more or less than the cash you actually received.

Franking Credits: The Major Tax Advantage of Australian ETFs

Franking credits are the single biggest tax advantage available to Australian ETF investors. When an Australian company like BHP or CBA pays corporate tax at 30%, it attaches "franking credits" to its dividends. These credits flow through the ETF to you, and you can use them to offset your personal tax bill.

Franking Levels by ETF

ETF | Category | Franking Level | Distribution Yield | MER |

|---|---|---|---|---|

AU High Yield | 88% | 7.9% | 0.25% | |

AU Shares (ASX 300) | 74% | 3.2% | 0.07% | |

AU Shares (ASX 200) | 72% | 3.0% | 0.04% | |

AU Shares (ASX 200) | 70% | 3.4% | 0.05% | |

AU Shares (ASX 200) | 66% | 3.3% | 0.05% | |

AU High Yield | 61% | 13.1% | 0.20% | |

International Shares | 0% | 1.8% | 0.18% | |

IVV (ASX) | S&P 500 | 0% | 0.8% | 0.04% |

Nasdaq 100 | 0% | 0.4% | 0.48% |

Why the difference? Franking credits only exist on Australian company dividends. VHY has the highest franking (88%) because it specifically targets high-dividend AU companies that pay heavily franked dividends — banks, miners, Telstra. International ETFs like VGS, IVV, and NDQ have zero franking because their underlying companies don't pay Australian corporate tax.

Why VAS has higher franking than IOZ: VAS tracks the ASX 300 (more small-mid caps), while IOZ tracks the ASX 200. The extra 100 small caps in VAS tend to include more fully-franking companies. Franking levels also vary quarter to quarter — these are trailing 12-month averages.

How Franking Credits Actually Save You Tax

This chart shows the effective tax rate on a $10,000 VAS distribution at 74% franking across every Australian tax bracket. The franking credit of $3,171 offsets your tax bill:

Your Marginal Rate | Tax Before Franking | Franking Offset | Net Tax / Refund | Effective Rate |

|---|---|---|---|---|

0% (under $18,200) | $0 | -$3,171 | Refund $3,171 | -31.7% |

16% ($18,201–$45,000) | $2,107 | -$3,171 | Refund $1,064 | -10.6% |

30% ($45,001–$135,000) | $3,951 | -$3,171 | Pay $780 | 7.8% |

37% ($135,001–$190,000) | $4,873 | -$3,171 | Pay $1,702 | 17.0% |

45% (over $190,000) | $5,927 | -$3,171 | Pay $2,756 | 27.6% |

The headline finding:

At the 0% tax rate (retirees, low-income earners, SMSF in pension phase), you get a cash refund of $3,171 on a $10,000 distribution. This is why retirees love franked dividends.

At the 16% rate, you still get a refund of $1,064.

At the 30% rate (most working Australians), your effective tax on the distribution drops to just 7.8% — compared to 30% if you received the same income unfranked.

Even at the top 45% rate, franking reduces your effective tax from 45% to 27.6%.

Franking credits make Australian equity ETFs dramatically more tax-efficient than international ETFs for income purposes.

Australian vs International ETF Tax: A Direct Comparison

This table compares the after-tax income on a $10,000 distribution from three different ETFs at a 30% marginal rate:

VAS (Australian shares): After franking offsets, you keep $9,220 of the $10,000. Net tax is just $780 (7.8% effective).

VGS (International shares, ASX-listed): No franking. You keep $7,280. The ~$280 foreign tax offset helps slightly, but you still pay $2,720 in tax.

VOO (US-listed, held directly): 15% US withholding tax reduces cash received to $8,500. FITO offsets $1,500. After-tax: $8,500.

VAS delivers $1,940 more after-tax income than VGS on the same $10,000 distribution. That's the power of franking credits.

International ETFs: Withholding Tax Explained

When you hold international ETFs like VGS or IVV on the ASX:

The US (or other country) government charges withholding tax on dividends paid to the ETF

Australia has a Double Tax Agreement with the US that reduces the rate from 30% to 15%

The ETF handles this internally — you never deal with the IRS

You may receive a Foreign Income Tax Offset (FITO) on your AMMA statement to avoid being double-taxed

If you hold US ETFs like VOO directly (not on the ASX), you need to file a W-8BEN form with your broker to claim the reduced 15% rate. Without it, you'll be hit with 30% US withholding.

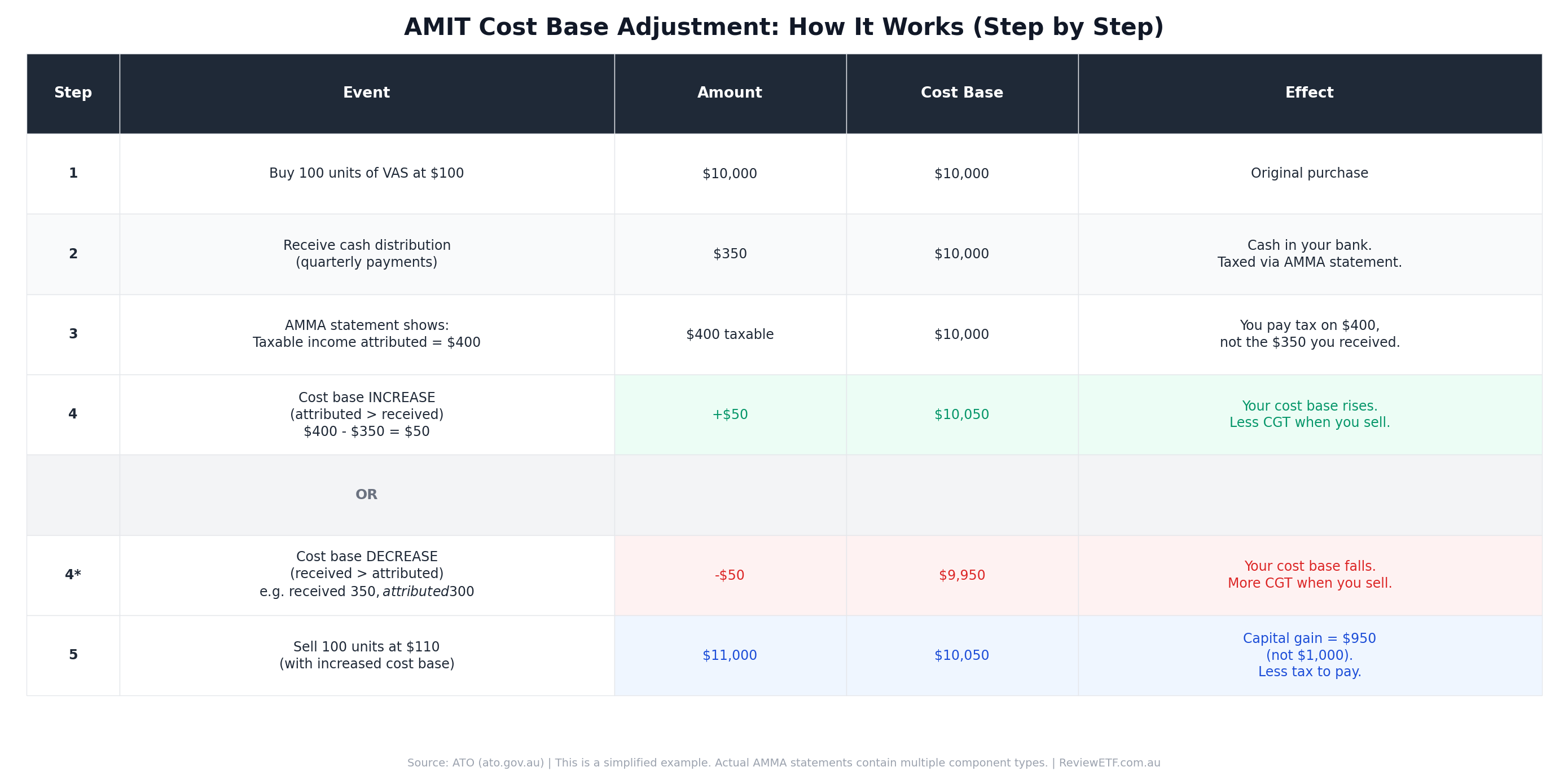

AMIT Cost Base Adjustments: The Part Everyone Gets Wrong

This is the most misunderstood part of ETF tax in Australia. Under the AMIT regime, the cash you receive in distributions is often different from the taxable amount attributed to you. The difference adjusts your cost base:

Taxable amount > Cash received → Cost base increases. You paid tax on income you didn't receive as cash. When you sell, your capital gain is smaller (or loss bigger). This is good.

Cash received > Taxable amount → Cost base decreases. You received more cash than was taxable. When you sell, your capital gain is larger. This means tax was deferred, not avoided.

Why It Matters

If you ignore AMIT cost base adjustments and just use your original purchase price when calculating CGT, you will either:

Overpay tax (if your cost base should have increased)

Underpay tax (if your cost base should have decreased — and the ATO will catch this)

Your cost base adjustments are listed on your AMMA statement each year. If you use Sharesight, they automatically load AMIT components for most major ETFs. Otherwise, you need to track these manually.

CGT Event E10: When Your Cost Base Hits Zero

If repeated cost base decreases reduce your cost base to zero, a CGT event E10 is triggered. Any further excess becomes a capital gain in that year. This is rare for broad index ETFs but can happen with high-distribution funds held for a very long time.

Capital Gains Tax on Selling ETFs

When you sell ETF units at a profit, you pay Capital Gains Tax. The rules are straightforward:

Scenario | Tax Treatment |

|---|---|

Held less than 12 months | Full capital gain added to taxable income |

Held 12 months or more | 50% CGT discount — only half the gain is taxable |

Sold at a loss | Capital loss can offset gains from other assets. Unused losses carry forward indefinitely |

DRP (reinvested) units | Each DRP reinvestment is a separate parcel with its own purchase date and cost base |

Critical detail: If you use a Distribution Reinvestment Plan (DRP), every quarterly reinvestment creates a new parcel. You need to track each one separately for CGT purposes. Selling 100 units might involve 20+ different parcels acquired at different prices on different dates.

The 12-month rule: You need to hold for at least 12 months (excluding both the purchase and sale date) to qualify for the 50% CGT discount. According to the ATO, this means a minimum of 367 days (368 in a leap year). Missing it by one day means no discount.

Tax Tips for ETF Investors

1. Don't sell ETFs just before the distribution date

If you buy an ETF just before the ex-distribution date, you'll receive the distribution — but it's not free money. The unit price drops by roughly the distribution amount on the ex-date. You've just received taxable income and triggered a cost base event. If you were planning to sell anyway, sell before the ex-date to avoid unnecessary tax.

2. Use DRP carefully

DRP is convenient but creates tax complexity. Each reinvestment is a taxable event (the distribution) AND creates a new CGT parcel. If you're disciplined about record-keeping, DRP is fine. If you're not, consider taking distributions as cash and manually reinvesting.

3. Australian equity ETFs are most tax-efficient for income

If you need regular income from your portfolio, Australian equity ETFs (VAS, A200, VHY) are dramatically more tax-efficient than international ETFs. The franking credits reduce your effective tax rate by 20+ percentage points.

4. International ETFs are better for growth accumulation

If you don't need income and are reinvesting everything, international ETFs like VGS or IVV have lower distribution yields, which means less annual tax to pay. The returns compound inside the fund. When you eventually sell, you get the 50% CGT discount (if held 12+ months).

5. Track your AMIT adjustments every year

Don't wait until you sell to figure out your cost base. Update your records every July/August when you receive your AMMA statement. Tools like Sharesight and Navexa handle this automatically for most Australian ETFs.

6. Consider the order you sell

Under the ATO's rules, you can use either FIFO (first in, first out) or specific identification to determine which parcels you're selling. If you have parcels with different cost bases, choosing the right method can significantly affect your CGT bill.

The Tax-Efficient ETF Portfolio

Based on the tax rules above, a tax-efficient approach for most Australian investors:

Role | ETF | Why It's Tax-Efficient |

|---|---|---|

AU core | 72-74% franking, lowest MER, broad diversification | |

Income | 88% franking, highest yield + franking combo | |

Global core | Low distributions = less annual tax. Growth compounds internally | |

US exposure | IVV (ASX) | ASX-listed wrapper avoids US estate tax and W-8BEN hassle |

For accumulation phase investors (building wealth, not drawing income), minimising distributions is more tax-efficient. For drawdown phase investors (retirees), maximising franked income is the priority.

Research every ETF mentioned in this article on ReviewETF — compare fees, performance, holdings, and distribution data across all 464 ASX-listed ETFs.

Sources: Australian Taxation Office (ATO), VanEck ETF Tax Guide, State Street Tax Tips, Vanguard, BetaShares, iShares, SPDR fund pages, Sharesight AMIT data, Pearler distribution comparisons. Franking levels based on trailing 12-month distributions as at February 2026.

No fund manager wrote this article. No issuer is paying for placement. This is independent analysis based on publicly available data.

This article is general information only and does not constitute financial or tax advice. Tax rules are complex and individual circumstances vary. Consider consulting a qualified tax adviser before making investment decisions based on tax considerations.