Hedged vs Unhedged ETFs: When to Use Each (and the Hidden Cost of Getting It Wrong)

Currency is the biggest hidden factor in your international ETF returns. Over the past 5 years, the falling Australian dollar added up to 43 percentage points of bonus return for unhedged investors. But in the last 12 months, the AUD rallied — and unhedged ETFs gave back 12–14% compared to their hedged equivalents.

We analysed 4 hedged/unhedged ETF pairs on the ASX to answer: when should you hedge, when should you not, and how much does it actually cost to get it wrong?

The Great Reversal

The same underlying shares. The same index. The only difference is currency hedging. Yet the return gap is enormous — and it completely reversed in the last year.

Pair | 5-Year Return (Unhedged) | 5-Year Return (Hedged) | Unhedged Lead |

|---|---|---|---|

+92.5% | +71.0% | +21.6% | |

+107.0% | +63.6% | +43.4% | |

+107.9% | +77.3% | +30.6% | |

+100.2% | +74.8% | +25.4% |

Over 5 years, unhedged won convincingly — by 21 to 43 percentage points depending on the pair. But zoom into the last 12 months:

Pair | 1-Year Return (Unhedged) | 1-Year Return (Hedged) | Hedged Lead |

|---|---|---|---|

VGS / VGAD | +7.1% | +19.9% | +12.8% |

IVV / IHVV | +3.5% | +17.8% | +14.3% |

NDQ / HNDQ | +6.0% | +20.3% | +14.3% |

QUAL / QHAL | +3.7% | +16.2% | +12.5% |

The hedged versions crushed unhedged by 12–14% in the last year. If you bought IVV (unhedged) twelve months ago, you got +3.5%. If you'd bought IHVV (hedged), you got +17.8%. Same shares. Same index. 14.3% difference — entirely from currency.

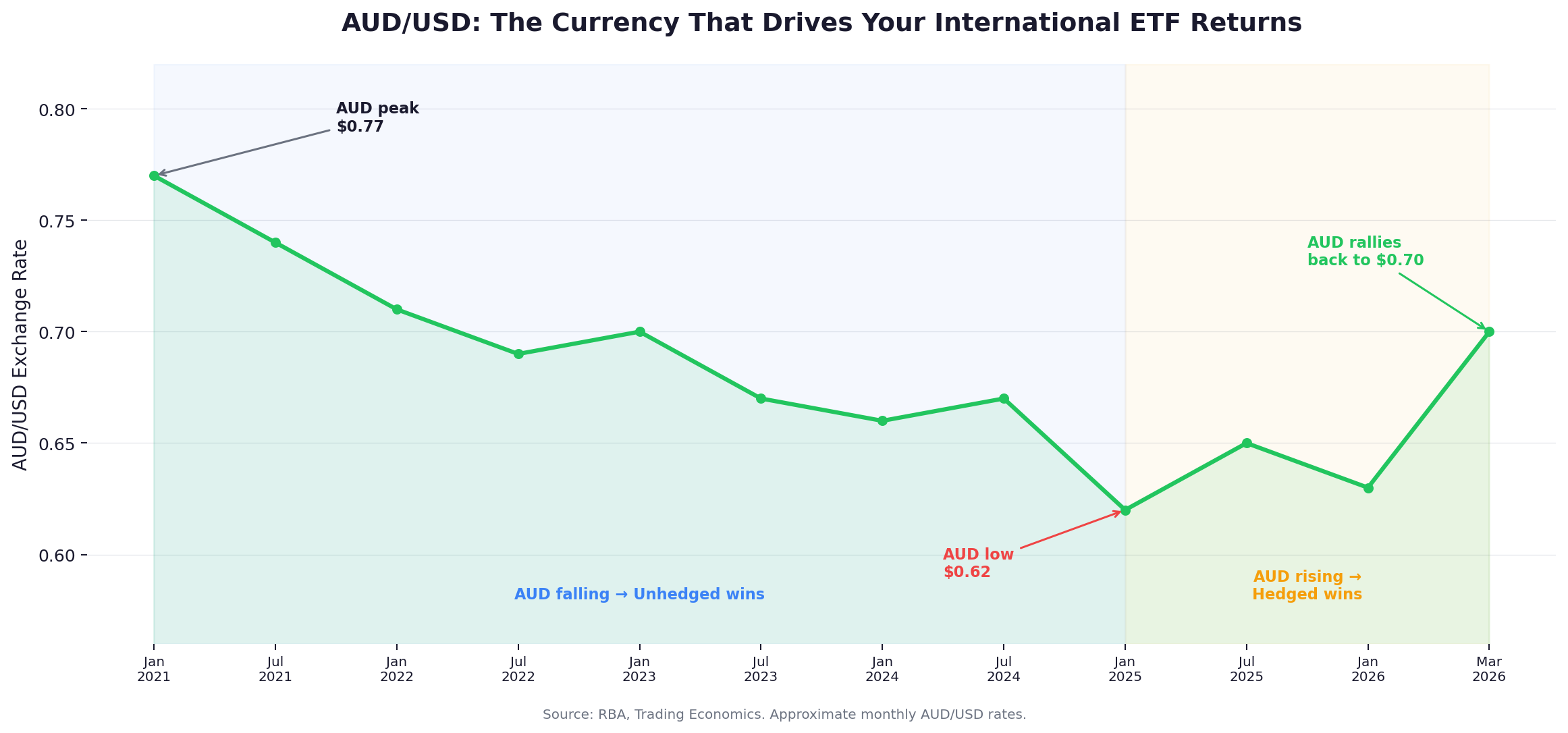

Why This Happened: The AUD Story

The AUD/USD exchange rate tells the whole story:

Period | AUD/USD | Direction | Who Won |

|---|---|---|---|

Jan 2021 | $0.77 | — | — |

Jan 2022 | $0.71 | Falling | Unhedged |

Jan 2023 | $0.70 | Still falling | Unhedged |

Jan 2024 | $0.66 | Still falling | Unhedged |

Jan 2025 | $0.62 | Multi-year low | Unhedged (peak advantage) |

Mar 2026 | $0.70 | Rallied 13% from low | Hedged |

The AUD fell from $0.77 to $0.62 over four years (2021–2025). Every cent the AUD falls adds roughly 1.5% to your unhedged return — because your US dollars are now worth more when converted back to AUD. Over this period, that currency tailwind added enormous bonus returns for anyone holding VGS, IVV, or NDQ unhedged.

Then the AUD reversed. From $0.62 in January 2025 to $0.70 in March 2026 — a 13% rally. That rally wiped out years of currency gains for unhedged investors and handed the advantage to hedged ETFs.

How Much of Your Return Was Currency?

The S&P 500 case study is the most stark:

IVV (unhedged) returned +107.0% over 5 years

IHVV (hedged) returned +63.6% over the same period

The difference: 43.4 percentage points — all currency

That means 41% of the unhedged S&P 500 return came from the falling AUD, not from US stock market gains. Investors who thought they were brilliant stock-pickers were partly just riding a currency wave.

The same pattern applies across all pairs:

Pair | Total Unhedged Return | Pure Equity Return (Hedged) | Currency Contribution | Currency as % of Total |

|---|---|---|---|---|

IVV / IHVV | +107.0% | +63.6% | +43.4% | 41% |

NDQ / HNDQ | +107.9% | +77.3% | +30.6% | 28% |

QUAL / QHAL | +100.2% | +74.8% | +25.4% | 25% |

VGS / VGAD | +92.5% | +71.0% | +21.6% | 23% |

Between a quarter and 41% of every unhedged international ETF's 5-year return was currency, not equity performance.

The Recent Pain: What AUD Strength Cost Unhedged Investors

Over the last 12 months, the AUD rose ~10% against the USD. That 10% AUD rally directly reduced unhedged returns by roughly 10–14 percentage points:

IVV investors got +3.5% when IHVV investors got +17.8%

VGS investors got +7.1% when VGAD investors got +19.9%

NDQ investors got +6.0% when HNDQ investors got +20.3%

On a $100,000 portfolio, the difference between hedged and unhedged in the last year was $12,500 to $14,300. That's not a rounding error — it's a material impact on wealth.

The Hedged/Unhedged Pairs Available on the ASX

Unhedged | Hedged | Exposure | Unhedged MER | Hedged MER | Fee Difference |

|---|---|---|---|---|---|

MSCI World ex-AU | 0.18% | 0.21% | +0.03% | ||

S&P 500 | 0.04% | 0.10% | +0.06% | ||

V500 | V5AH | S&P 500 (Vanguard) | 0.07% | 0.09% | +0.02% |

Nasdaq 100 | 0.48% | 0.51% | +0.03% | ||

MSCI World Quality | 0.40% | 0.43% | +0.03% | ||

VTEK | VTKH | Global Technology | 0.23% | 0.26% | +0.03% |

Hedging costs 0.02–0.06% more in MER. That's tiny compared to the 12–43% swings that currency movements can cause.

When to Hedge and When Not To

✅Hedge when:

You believe the AUD will strengthen (or you have no view and want to remove the risk). If the AUD rises from $0.70 to $0.80, unhedged investors lose roughly 12% from currency alone.

You're investing for a specific AUD-denominated goal (house deposit, retirement income). You don't want currency volatility affecting the value of your goal.

You're investing short to medium term (1–5 years). Currency swings are large relative to equity returns over shorter periods. Over 1 year, currency can easily be the dominant factor.

You want pure equity exposure. If you're buying the S&P 500 for the US equity return, hedging gives you exactly that — without the currency bet on top.

❌Don't hedge when:

You believe the AUD will weaken (or you want the natural diversification). When the AUD falls, your overseas holdings are worth more in AUD.

You're investing long term (10+ years). Over very long periods, currency tends to mean-revert. The AUD doesn't go to zero or infinity — it oscillates. Hedging costs compound every year while currency effects wash out.

You want a natural hedge against Australian economic risk. If Australia enters a recession, the AUD typically falls — which boosts your unhedged international holdings precisely when your Australian assets are struggling. That's a valuable natural diversification.

You can't be bothered managing it. The default recommendation for most long-term investors is unhedged, because it's simpler and the currency effects tend to cancel out over decades.

🌓 The split approach:

Many advisers recommend a 50/50 split between hedged and unhedged for international exposure. This way you're half right regardless of which way the AUD moves. If you hold 70% international:

35% unhedged (VGS or IVV)

35% hedged (VGAD or IHVV)

This eliminates the need to predict currency direction while still getting some natural diversification benefit.

The Verdict

➡️Currency is not a minor factor — it's a major one. Over the past 5 years, it accounted for 23–41% of every unhedged international ETF's return. In the last 12 months, it swung the other way and cost unhedged investors 12–14%.

➡️Most Australian investors are 100% unhedged because that's what the finfluencers recommend (VGS, not VGAD). That worked brilliantly from 2021–2024 when the AUD was falling. It has not worked in the last year.

➡️There's no permanently right answer. Hedging is not free — it costs 0.02–0.06% per year and removes the natural diversification benefit. But being 100% unhedged is a bet that the AUD will stay weak or weaken further. If you don't have a strong view on currency, consider splitting your international exposure between hedged and unhedged. The data shows the swings are too large to ignore.

Research every ETF mentioned in this article on ReviewETF — compare fees, performance, and holdings across all 464 ASX-listed ETFs.

Sources: CBOE Australia Monthly Funds Report (February 2026), RBA Exchange Rates, Trading Economics, Vanguard Australia, BlackRock Australia, BetaShares, ReviewETF.com.au.

No fund manager wrote this article. No issuer is paying for placement. This is independent analysis based on publicly available data.

This article is general information only and does not constitute financial advice. Consider your own circumstances and seek professional advice before making investment decisions.