The right ETF at 25 is the wrong ETF at 65. A young investor with decades ahead should take maximum risk. A retiree drawing income needs stability. The data is unambiguous on this — and the cost of getting it wrong is enormous.

We modelled real ASX ETF returns across five risk profiles to show exactly what happens at each life stage, and how much it costs if your portfolio doesn't match your time horizon.

The Spectrum: Five Risk Profiles

There are five diversified ETFs on the ASX that form a clean risk spectrum — from 100% growth to 30% growth. Each one is a single-fund portfolio.

ETF | Growth / Defensive | MER | 5Y Annualised Return | Best For |

|---|---|---|---|---|

100% / 0% | 0.19% | 11.3% p.a. | Ages 20–35 | |

90% / 10% | 0.27% | 9.4% p.a. | Ages 30–45 | |

70% / 30% | 0.27% | 7.3% p.a. | Ages 45–60 | |

50% / 50% | 0.27% | 5.1% p.a. | Ages 55–65 | |

30% / 70% | 0.27% | 3.3% p.a. | Income drawdown phase |

Every step down the risk ladder costs you return. The question is whether that's a price worth paying at your stage of life.

Stage 1: Ages 20–40 — Maximum Growth

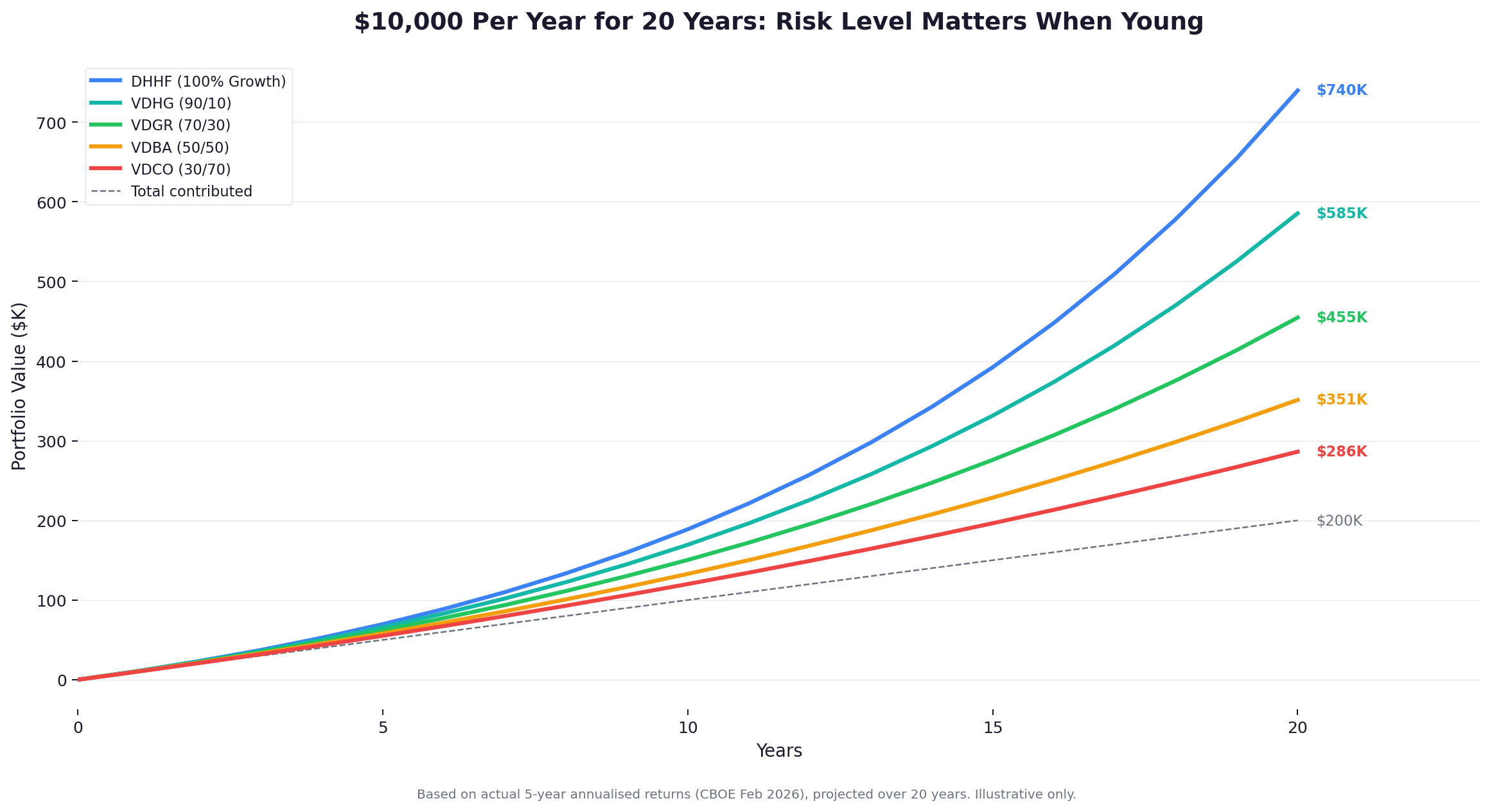

When you're young, you have one asset that no amount of money can buy: time. A 25-year-old investing $10,000 per year has 20+ years of compounding ahead. The data says go aggressive.

$10,000 Per Year for 20 Years

ETF | Risk Profile | Final Value | Growth on $200K Contributed |

|---|---|---|---|

100% growth | $740,000 | +$540K | |

90/10 | $585,000 | +$385K | |

70/30 | $455,000 | +$255K | |

50/50 | $351,000 | +$151K | |

30/70 | $286,000 | +$86K |

The cost of being too conservative when young is staggering. The difference between DHHF (100% growth) and VDCO (30/70) is $454,000 on the same $200,000 contributed. That's not a rounding error — it's a house deposit.

Why it works at this age: You have 20+ years to ride out downturns. Even the 2022 drawdown (-5% for DHHF) was recovered within a year. When you're not withdrawing, short-term volatility is irrelevant. Only the long-term compound rate matters.

The pick: DHHF (0.19%, 100% growth) or VDHG (0.27%, 90/10). If you want to build your own, pair A200 (Australian shares, 0.04%) with BGBL (international shares, 0.08%) in a 30/70 or 40/60 split for an even lower fee.

Stage 2: Ages 40–60 — Still Growing, Start Thinking

At 40–50, you likely have a larger portfolio and are earning more. You still have 15–25 years until retirement. The data says stay growth-oriented, but begin considering your transition plan.

The pick for 40–50: VDHG (90/10) or VDGR (70/30). The 10–30% defensive allocation provides a modest buffer without materially sacrificing returns. VDGR returned 7.3% p.a. — $455K on $200K contributed over 20 years. That's still strong compounding.

The pick for 50–60: Begin transitioning toward VDGR (70/30) or VDBA (50/50). The closer you get to retirement, the less time you have to recover from a bad year. A 30–50% drawdown five years before retirement is devastating. A 30% defensive allocation smooths the ride.

The transition doesn't need to be instant. You can gradually shift from VDHG to VDGR over a decade — or simply direct new contributions to the lower-risk fund while leaving existing holdings to compound.

Stage 3: Ages 60+ — Retirement and Drawdown

This is where the strategy fundamentally changes. You're no longer adding money — you're taking it out. The risk isn't volatility. The risk is running out of money.

$1M Portfolio, $50K/Year Withdrawal — How Long Does It Last?

Strategy | Avg Return | After 30 Years |

|---|---|---|

DHHF (100% growth) | 10.0% | $7.4M (still growing) |

Cash Buffer + VDGR | 6.2% | $1.65M (stable) |

VDGR (70/30) | 6.2% | $1.78M (still growing) |

VDBA (50/50) | 4.4% | $288K (just surviving) |

Cash Only (AAA) | 3.0% | Ran out after 31 years |

The pure cash strategy runs out. VDBA barely survives. But anything with 70%+ growth allocation comfortably sustains $50K/year withdrawals over 30 years — and actually grows the portfolio.

The Cash Buffer Strategy

The smartest retirement approach isn't "go conservative" — it's growth assets with a cash buffer. Here's how it works:

Hold 90% in VDGR (70/30 growth)

Hold 10% in cash (AAA or a high-interest savings account) — roughly 2 years of living expenses

In up years — withdraw from VDGR, top up the cash buffer

In down years — withdraw from cash, let VDGR recover

This does two things:

You never sell growth assets in a downturn (which locks in losses)

You always have 2 years of cash to ride out any market crash

The modelled result: $1M grew to $1.65M over 30 years while withdrawing $50K/year. The cash buffer cost roughly $130K vs holding 100% VDGR — that's the insurance premium for sleeping at night.

Why Not Go 100% Conservative?

The data is brutal on this. A 100% cash portfolio ($1M in AAA) runs out after 31 years at $50K/year withdrawals. With inflation, it effectively runs out even sooner. Conservative feels safe — but it's actually the riskiest strategy over a 25–30 year retirement because it guarantees your portfolio won't keep up.

The Life Stage Summary

Age | ETF | Allocation | Why |

|---|---|---|---|

20–35 | 100% growth | Maximum time to compound. Volatility is irrelevant. | |

35–45 | 90% growth / 10% defensive | Still decades ahead. Small buffer, minimal return sacrifice. | |

45–55 | 70% growth / 30% defensive | Approaching retirement. Smooth the ride. | |

55–65 | VDGR + cash buffer | 70% growth + 2yr cash | Transition to drawdown. Cash buffer protects against sequence risk. |

65+ | VDGR + cash buffer | 70% growth + 2yr cash | Sustain withdrawals for 30 years. Don't go too conservative. |

The key insight: You need growth assets in retirement. Going 100% conservative is a trap — it feels safe but guarantees you run out of money faster. A 70/30 growth allocation with a 2-year cash buffer is the sweet spot: enough growth to sustain 30 years of withdrawals, enough cash to avoid selling in a crash.

The DIY Alternative

If you'd rather build your own portfolio than use an all-in-one fund, here are the building blocks at each stage:

Young (20–40): Maximum Growth

ETF | Role | Allocation | MER |

|---|---|---|---|

Australian shares | 30–40% | 0.04% | |

International shares | 60–70% | 0.08% | |

Blended MER | ~0.07% |

This is essentially DHHF's exposure for roughly a third of the fee. The trade-off is you need to rebalance periodically.

Retirement (60+): Growth + Buffer

ETF | Role | Allocation | MER |

|---|---|---|---|

Australian shares | 25% | 0.04% | |

International shares | 45% | 0.08% | |

Australian bonds | 20% | 0.10% | |

Cash buffer (2yr) | 10% | 0.18% | |

Blended MER | ~0.08% |

Research every ETF mentioned in this article on ReviewETF — compare fees, performance, and holdings across all 464 ASX-listed ETFs.

Sources: CBOE Australia Monthly Funds Report (February 2026), Vanguard Australia, BetaShares, ReviewETF.com.au. Models use actual 5-year annualised returns projected forward — past performance is not a guarantee of future results.

No fund manager wrote this article. No issuer is paying for placement. This is independent analysis based on publicly available data.

This article is general information only and does not constitute financial advice. Consider your own circumstances and seek professional advice before making investment decisions.